Up Next

There’s never been a better time to own a Formula 1 team, but as the good times roll in Haas is in danger of missing out thanks to underinvestment that risks making it forever the poor relation on the grid.

It’s time for owner Gene Haas either to put up, by maximising the allowed investment in the team, or get out by selling on to someone who will.

There is, of course, a middle way whereby a minority stake can be sold to raise funds for the necessary spending.

Alpine, for example, sold 24% of its F1 team to an investment group but retains control.

But the point is that Haas has a fantastic opportunity and risks squandering it.

It’s easy to criticise Haas given its poor on-track performance in 2023, but that’s not the main symptom of the problem.

Instead, you have to ask whether a team that did a remarkable job to establish itself in F1 during far more difficult financial times, and survived its brush with oblivion during the COVID-19 pandemic, is wasting the opportunity F1’s recent growth presents.

HOW MUCH IS HAAS ACTUALLY WORTH?

Haas F1 is still worth big money thanks to being only one of 10 F1 teams.

Earlier this year, Forbes estimated the value of the team at $780million and as there is no lack of aspiring investors searching for opportunities to buy into teams, or even acquire them outright, there’s no reason why that value couldn’t be realised.

For sufficiently motivated buyers, and there’s a few of those around, it could even be higher.

But it’s not just F1’s popularity that’s driving the talk of multi-billion-dollar teams.

The prevailing financial conditions, notably the cost cap, set at a baseline of $135m per season, and the more equitable distribution of the slice of F1’s revenue shared by the teams means the economic foundations are better than they have been for decades - perhaps ever given the potential rewards on offer.

The conditions are therefore perfect for Haas.

When it joined the grid in 2016, spending was unlimited - meaning that even hefty investment could represent only a drop in the ocean.

Therefore, you could pour hundreds of millions into your team year after year and see little or no yield in terms of either competitiveness or value.

Owner Gene Haas publicly questioned whether it was worth continuing given the struggle to get sponsors, suggesting that after five years competing it might be time to stop.

That was before the COVID-19 pandemic hit, with the financial impact meaning that Haas’s future looked bleak.

But having weathered that storm thanks to team principal Guenther Steiner’s strategy of minimising investment in on-track performance in the rest of 2020 and 2021, along with taking on drivers who brought money - notably Nikita Mazepin and his Uralkali money - Haas survived.

The new, more favourable, Concorde Agreement was signed and a team that could realistically have been closed down made it to F1’s brave new financial world.

What’s more, the team was in a better position technically with the establishment of a design office in Maranello under technical director Simone Resta.

It retains a technical partnership with Ferrari, which provides all the components that are permitted under the regulations, and continues to be allied with Italian chassis manufacturer Dallara, but today Haas is more of a ‘complete’ F1 team than it has ever been.

Now, Haas must build on that and the full funding does not appear to be there to do so.

HOW RIVALS ARE LEAVING HAAS BEHIND ON SPENDING

To maximise the performance potential of an F1 team, it’s necessary not just to be at the limit of cost cap spending, and Haas was close this year, but also the permitted capital expenditure.

That allowance was recently increased by a further $20m, which can be invested in infrastructure and key tools.

Haas’s direct rivals are spending big.

AlphaTauri is upgrading its facilities by moving some of its operation to Red Bull’s Milton Keynes campus, Sauber is benefitting from Audi money and Williams is gradually growing under sustained spending from Dorilton Capital.

Haas needs to keep pace or risk falling behind. Despite landing some lucrative partners, such as title sponsor MoneyGram and new arrival Play’n Go, Haas is unlikely to have the capital to match them all.

Finishing last in the constructors’ championship when it was in the mix to finish as high as seventh, which represents a difference of approximately $30m given there’s around $10m difference per position in prize money, is also a big blow.

Given Haas was eighth in 2022, that means one income source is slashed by about $20m.

There is unlikely to be a top up to compensate for that, so it’s going to be dependent on bringing in more money to get close to the investment level needed do more than tread water.

DOES THE HAAS TEAM DESERVE EXTRA FUNDING?

“We just need to make it up,” Steiner tells The Race when asked about the financial impact of finishing last.

“We found more partners. We announced Play’n Go, in Las Vegas, they are big partners and they help making up the losses.

“But in the end we need to see where we find the additional financing.”

However, Steiner also defends the team’s position on the basis that it’s all well and good throwing cash in but it depends on investing it properly.

“I look back to the old days, when people said money makes you the best team, it didn’t because some people spent a lot of money and didn’t win anything, so you need to be careful,” says Steiner.

“It needs to be not expenditure, but investment. That’s the key word here. What do you invest to get better?

“It’s not that you get a return tomorrow, it takes time. A lot of people speak about investment and it’s a lot of propaganda, it’s about whether the investment works out.”

That’s true, but you cannot always count on rivals squandering investment. Haas needs to keep pace if it’s to have the chance to be more than a perennial back-of-the-grid operation.

You could argue that Gene Haas would be within his rights to cite the team’s current underachievement as evidence that the investment level is not the problem.

He’d be right insofar as its 2023 struggles aren’t a direct result of that given there’s no question it had the resources to do significantly better.

However, that would neglect the big picture.

HOW HAAS SQUANDERED ITS 2023 POTENTIAL

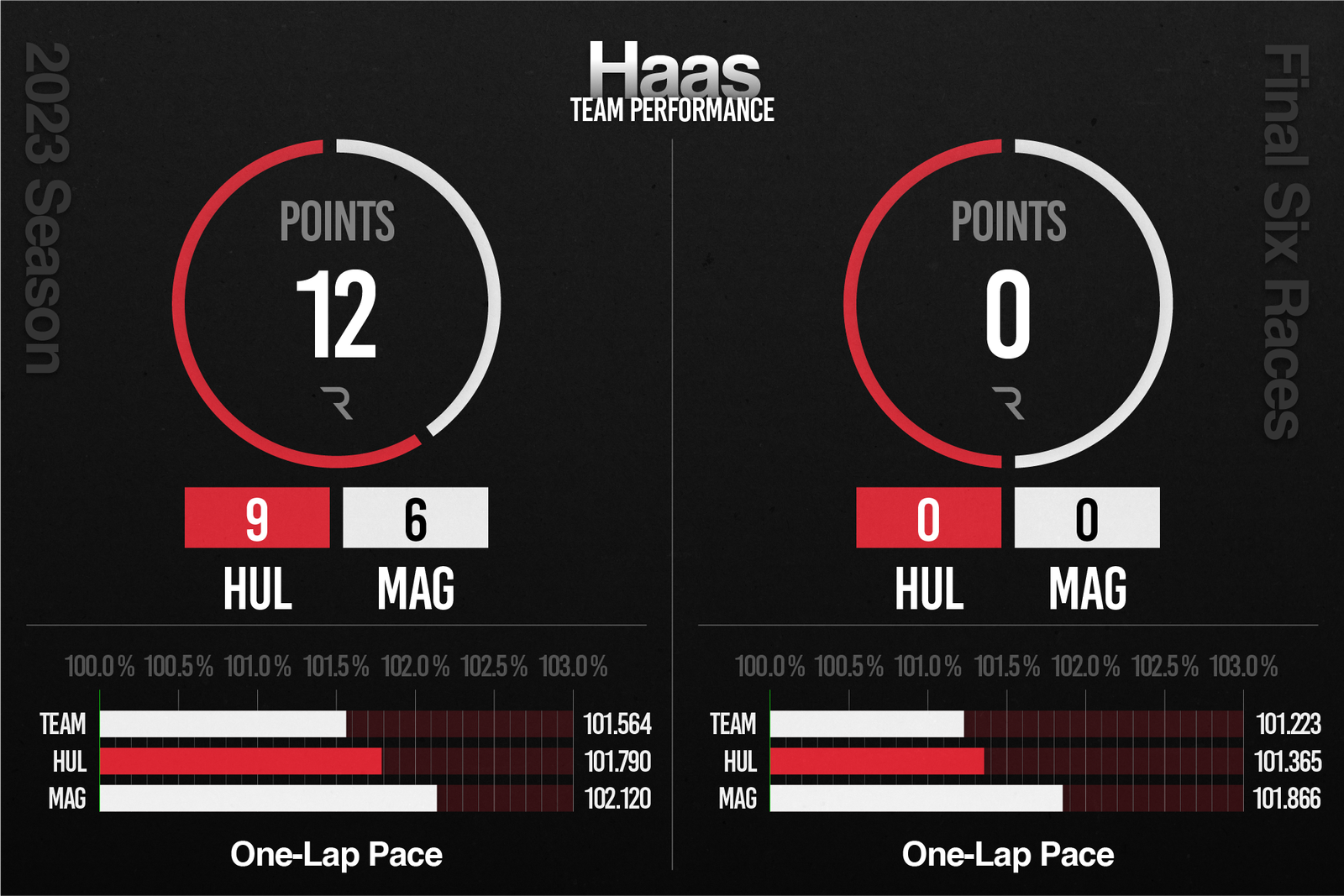

The 2023 Haas was brisk over a lap but ate its tyres in race stints, meaning points were rare.

That was the consequence of some flat-footed technical decision-making and the failure to change the aerodynamic design direction until months of stagnation in finding performance in the windtunnel.

That new direction yielded a hastily designed change in aerodynamic concept introduced late in the season that wasn’t an instant hit, but that the team hopes will have accelerated its learning curve to feed knowledge into the 2024 car.

“We got hit pretty badly with not making progress in development,” says Steiner. “We put all the effort in, there was no limitation on effort, and we had the budget to do upgrades.

"Everybody thinks we don't do upgrades because we don't have the money but we didn't find any performance, that was the biggest thing.

“And the other thing was that when we realised, it was a little bit late and we should have to caught that earlier.

"We just need to get better in the windtunnel, otherwise the team is not too bad. It could always be better, but it’s just that we didn’t find anything.”

WHAT DOES THE IDEAL FUTURE LOOK LIKE FOR HAAS?

There’s no immediate intention to strike out on its own rather than relying on Ferrari for the majority of its car, which is a sensible strategy that allows Haas to focus on making improvements with its production of the listed team parts that make the big difference in terms of performance.

And there’s no doubt whatsoever that the problems in 2023 were aerodynamic, not mechanical.

However, there’s still plenty that can be done within the current business model.

And that’s what Gene Haas should be investing in so that the team not only maximises its performance under its current constraints, but can be in a position to grow long term along with its rival teams.

“At the moment, the best way for us is to keep the same business model because if you change it you need to do it slowly,” says Steiner.

“The difficulty we have is that if we try to take on more work, it wouldn’t go well because you normally take a step back before you go two forward if you completely change.

“In the short term, we stay with the same business model.

“There are pros and cons to this model. For example, we don’t have a 60% windtunnel and investing $50m to build a windtunnel in 2023 is a difficult task because windtunnels will be around, but not forever.

"And Gene already has a windtunnel, Windshear, but that’s a 100% one and asking him to buy another windtunnel is a stiff demand.

"The Ferrari windtunnel is good, so we have a known quantity and why change that?

"It’s more important for us to look over the parts we make, the aero. The problem is not the business model.

“We need to exploit the potential of the business model we have at the moment, which we are not because we are last in the championship.

"There is more in it than that. Can you win a world championship with our business model? I don’t think so, but can you be fifth? Yes, because we did it before.”

Next season should be better for Haas and there’s no reason why it can’t finish higher in the championship.

That’s the current short-term goal, to make the most of the aerodynamic capacity it has got.

But hand-in-hand with that must go the evolution of the team, and that’s going to require maximising the investment.

One visually obvious example of where it falls behind is its motorhome in the paddock, which it has used since 2016.

While that might not seem relevant to the performance of the car, when you are trying to bring in partners and you have comfortably the smallest facility in the paddock it makes a visual statement.

These are the areas where money could be spent for positive effect and it would probably only require an extra $50-100m over the coming years to ensure the growth rate is maximised.

What’s frustrating to those who have followed the Haas story for the past decade is that it has achieved so much and has survived against the odds, yet risks not taking the final step to ensure not just to maximise its value, but also its performance potential.

Ultimately, it’s Gene Haas’s choice given he’s the owner of the team, but it seems perverse to go through all that and invest so much then neither pump in what is relatively speaking a small sum to go the final mile, nor sell up to let someone else do it.